No theatrics, just the facts you need to protect your health, your benefits, and your case. Florida’s Personal Injury Protection (PIP) is a No-Fault system with a strict 14-day rule. If you don’t get evaluated by an approved provider within 14 days of a crash, your PIP Insurer can deny benefits entirely.

Table of Contents

- What “PIP” Covers (and What it Doesn’t)

- The 14-Day Rule: What Counts as “Initial Services”?

- EMC vs. Non-EMC: Why $10,000 Can Drop to $2,500

- Who Can Diagnose EMC?

- Approved Providers vs. Excluded Services(Massage/Acupuncture)

- Timelines After Day 1: Provider Billing, Insurer Deadlines, and Your Role

- Step-by-Step: What to do in the First 14 Days

- How McKyton Law Uses Early Evidence to Build Leverage

- Common Pinella County Scenarios

- FAQ: St. Petersburg Car Accident Lawyer Answers

What “PIP Covers (and What it Doesn’t)

Florida requires PIP on most personal auto policies. In a typical auto accident, PIP pays 80% of reasonable medical bills, 60% of lost wages, and a death benefit, up to your policy limit, usually $10,000, regardless of fault. That’s the No-Fault insurance piece: your carrier pays first, then other claims may follow.

Two practical limits matter immediately:

- The 14-Day Rule. If you don’t obtain initial medical services within 14 days, PIP benefits can be denied entirely.

- EMC vs. non-EMC. Without a qualifying Emergency Medical Condition (EMC), PIP medical benefits may cap at $2,500 instead of $10,000.

The 14-Day Rule: What Counts as “Initial Services” for PIP

Under Fla. Stat. § 627.736, your initial services and care must be rendered within 14 days of the crash and by an approved provider type (see examples below). This can be an ER visit, urgent care, a primary-care physician, a doctor of osteopathy, a chiropractor, a dentist (think jaw/tooth impact), or emergency transport.

** Call it day one at the scene; your job is to get medically evaluated and start the paper trail. Delaying risks both your health and your PIP claim.

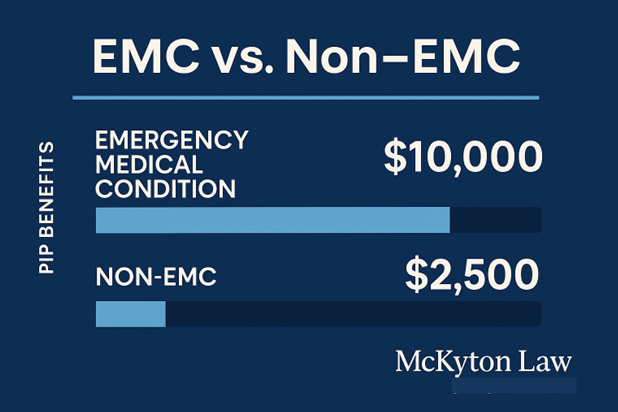

EMC vs. non-EMC: Why $10,000 can Drop to $2,500 In a Personal Injury Case

To access the full $10,000 in PIP medical benefits, your injury must qualify as an Emergency Medical Condition (EMC): a statutorily defined condition with acute symptoms that could reasonably lead to serious jeopardy, impairment, or dysfunction without immediate attention. If no EMC is determined, POP medical benefits are often limited to $2,500.

Key Points:

- The EMC decision does not have to be made within the first 14 days; the statute requires initial treatment within 14 days, but EMC can be established later in the course of care by the proper provider.

- If your injuries seem minor at first, follow-up and re-evaluation can be critical. Soft-tissue pain, concussion symptoms, or spine complaints can evolve; document them as they develop.

Who Can Diagnose an EMC Following a Car Accident?

Florida law defines EMC in Statute § 627.732 and ties PIP payment levels to that determination. In practice, the EMC determination must come from an M.D. (physician), D.O. (osteopath), dentist, or a comparable authorized provider under the statute; chiropractors can provide initial services, but cannot make an EMC determination for the full $10,000 medical benefit. (Your treating team will guide this; we make sure the right provider documents it in the record.)

Florida law defines EMC in Statute § 627.732 and ties PIP payment levels to that determination. In practice, the EMC determination must come from an M.D. (physician), D.O. (osteopath), dentist, or a comparable authorized provider under the statute; chiropractors can provide initial services, but cannot make an EMC determination for the full $10,000 medical benefit. (Your treating team will guide this; we make sure the right provider documents it in the record.)

Approved Providers vs. Excluded Services (Massage/Acupuncture)

Covered initial providers include hospital emergency departments, physicians, doctors of osteopathy, chiropractic physicians, dentists, and emergency transport. Massage therapy and acupuncture are explicitly not reimbursable under PIP, no matter who provides them. If your care plan includes these, understand that PIP won’t pay those line items.

Timelines After Day 1 of Your Car Accident: Provider Billing, Insurer Deadlines, and Your Role

Florida’s PIP statute includes strict billing and payment windows that operate behind the scenes, but they can affect your experience:

- Provider billing: Most medical providers must submit bills to the PIP insurer within 35 days of service (with a limited extension if they timely submit a notice of initiation of treatment). This is on the provider, not the accident victim.

- Insurer payment: After receipt of a proper bill, the insurer generally has 30 days to pay; unpaid bills become overdue and may trigger statutory remedies.

*Your job: keep appointments, save all paperwork (discharge instructions, prescriptions, work-status notes), and funnel everything to your attorney so the file stays tight and timelines don’t slip.

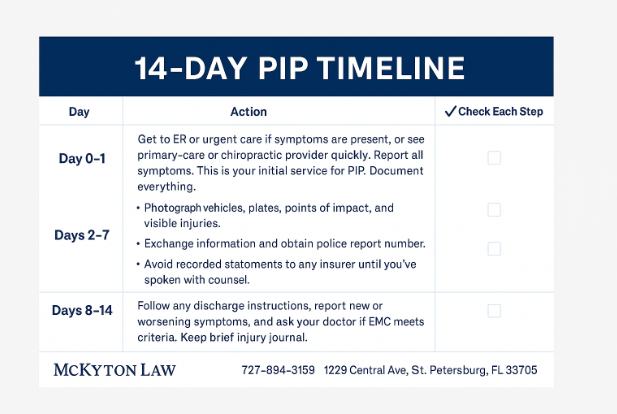

Step-by-Step: What to Do in the First 14 Days Following a Car Accident

Day 0-1: Safety, Documentation, Medical Intake

- Get to an ER or urgent care if symptoms are present, or see your primary care or chiropractic provider quickly. Tell them about all of your symptoms, even if mild. This is your initial service for PIP. Document everything.

- Photograph vehicles, plates, points of impact, and visible injuries.

- Exchange information and obtain the police report number.

- Avoid recorded statements to any insurer until you’ve spoken with a personal injury attorney.

Days 2-7: Follow-up and The Paper Trail

- If you left the ER with instructions to follow up, do it. New or worsening symptoms? Return or call your provider.

- Ask your treating physician/osteopath whether your findings meet EMC criteria. Early clarity helps ensure access to the full $10,000.

- Keep a brief injury journal (pain levels, sleep, work limits). Evidence today becomes leverage tomorrow.

Days 8-14: Lock in PIP Eligibility

- If you haven’t been seen yet, go now! You must receive initial services within 14 days. Don’t wait for a “big” symptom to appear.

- Confirm your providers are submitting bills correctly to your PIP insurer; while the billing duty is theirs, we like to verify so nothing falls through the cracks.

After Day 14:

You can still treat, of course. But if you missed the 14-day window for initial care, PIP benefits may be denied.

How McKyton Law Uses Early Evidence to Build Leverage For Personal Injury Protection

At McKyton Law, we don’t shout. We prepare. Our evidence-first approach is designed to make insurers see verdict risk and pay fair value, often without trial.

Medical Records Discipline: We help you get the right providers on record within 14 days, then coordinate follow-up so your file reflects causation, diagnoses, work limits, and future care in clear, insurer-recordable terms.

EMC Strategy: When the medicine supports it, we ensure an authorized provider documents an EMC determination so our medical benefits can access the full $10,000 PIP.

Damages Matrix: We track medical bills, EOBs, wage loss (PIP pays 60%), out-of-pocket costs, and the human impact; cleanly organized to shorten negotiation timelines.

Local Advantage: St. Petersburg and Pinellas County venues and mediators matter. We tailor demand packages to the decision-makers who’ll see them.

Common Pinellas County Scenarios Regarding Personal Injury Protection (PIP)

Rear-End Collision on 34th St.

You feel “okay” and go home. The next morning, neck spasm and headache hit. You must be seen within 14 days. Urgent care, PCP, or a chiropractic evaluation counts as initial services. If your symptoms meet EMC, your PIP medical benefits access the full $10,000; without EMC, medical payments may cap at $2,500. We coordinate with your providers to keep the record as light as possible.

Intersection T-Bone in Downtown St. Pete

EMS transports you to Bayfront. That ER visit is your timely initial service. Follow discharge instructions, and see the recommended specialists. We ensure your care is properly billed to PIP and wage loss is documented (PIP covers 60% of last wages up to policy limits).

Bicycle Struck by Rideshare on Central Ave.

Even if you weren’t driving, PIP may still apply depending on policy and household relationships. The Rule remains the same: 14-day initial care, then a medically grounded path to recovery and valuation. We sort the coverage priorities for you.

FAQ: St. Petersburg Car Accident Lawyer Answers’

Q: I felt fine at the scene and waited three weeks. Can I still use PIP?

A: Likely, no. If you did not receive initial services within 14 days, PIP can deny benefits. We’ll look at other coverages and potential liability claims to protect your recovery.

Q: Do I need to prove the other driver was at fault to use PIP?

A: No. PIP is No-Fault; your own policy pays first up to the limit (subject to EMC and other rules). Fault matters later for additional compensation.

Q: Who can declare an Emergency Medical Condition?

A: An M.D., D.O., or Dentist (among those authorized) can make the EMC determination used for PIP’s full-benefit level. Chiropractors can provide initial services, but not the EMC decision for full benefits.

Q: Will massage or acupuncture be covered?

A: No. The statute expressly excludes them from PIP reimbursement.

Q: What if my provider’s billing is late?

A: Florida law sets strict timelines (generally 35 days to submit, subject to limited extensions). That’s on the provider, not you, but late billing can complicate payment flow. We watch the file and step in when needed.

Q: How long do I have to file a separate injury claim if my damages exceed PIP?

A: Many negligence claims now have a two-year statute of limitations from the date of the crash (subject to exceptions). Don’t wait. Strategy and evidence age fast. (Talk with counsel about your facts.)

Why This Matters: Evidence – Leverage – Stronger Settlements in St. Petersburg Personal Injury Cases

Florida PIP’s 14-day Rule is more than a deadline. It’s the first test of file quality. Timely initial services, a clear EMC decision when appropriate, and disciplined documentation of medical bills and lost wages lead to fair outcomes for insurers. That’s our lane: No hype—all Proof.

About McKyton Law Firm

McKyton Law Firm represents individuals and families across St. Petersburg and Pinellas County in personal injury and wrongful death matters, including car, motorcycle, pedestrian, and commercial vehicle crashes. The firm combines thorough investigation, clear communication, and trial-ready preparation to pursue full and fair compensation for clients’ medical care, lost wages, and long-term needs. Consultations are free, and there are no fees unless we recover for you.